Intravascular Visualization Devices in 2025: Unveiling the Next Era of Cardiovascular Imaging. Explore how cutting-edge technology and clinical demand are driving double-digit growth and reshaping patient care.

- Executive Summary: Key Insights & 2025 Outlook

- Market Size & Growth Forecast (2025–2030): CAGR Analysis

- Technological Innovations: From IVUS to OCT and Beyond

- Competitive Landscape: Leading Manufacturers & New Entrants

- Clinical Applications & Evolving Use Cases

- Regulatory Environment & Standards (FDA, CE, etc.)

- Regional Market Dynamics: North America, Europe, Asia-Pacific

- Adoption Drivers: Precision Medicine & Minimally Invasive Trends

- Challenges & Barriers: Cost, Training, and Integration

- Future Outlook: Emerging Technologies & Strategic Opportunities

- Sources & References

Executive Summary: Key Insights & 2025 Outlook

Intravascular visualization devices, encompassing technologies such as intravascular ultrasound (IVUS), optical coherence tomography (OCT), and near-infrared spectroscopy (NIRS), are pivotal in advancing the precision and safety of cardiovascular interventions. As of 2025, the sector is experiencing robust growth, driven by the increasing global prevalence of cardiovascular diseases, the demand for minimally invasive procedures, and ongoing technological innovation. The integration of artificial intelligence (AI) and improved imaging algorithms is further enhancing the diagnostic and therapeutic capabilities of these devices.

Key industry leaders continue to shape the competitive landscape. Philips remains a dominant force, offering a comprehensive portfolio of IVUS and OCT systems, including the EPIQ CVx and Azurion platforms, which are widely adopted in catheterization laboratories worldwide. Boston Scientific is another major player, with its OPTICROSS IVUS and POLARIS imaging systems, and is actively investing in next-generation platforms that integrate real-time data analytics. Abbott continues to expand its presence with the OPTIS Integrated System, which combines OCT and angiography co-registration, enabling more precise lesion assessment and stent optimization.

Recent years have seen a surge in regulatory approvals and product launches. In 2024, Terumo Corporation received expanded clearances for its Ultimaster and Finecross MG IVUS catheters, targeting both coronary and peripheral vascular applications. Meanwhile, ACIST Medical Systems has advanced its HDi IVUS platform, focusing on high-definition imaging and workflow integration. These developments underscore the sector’s commitment to improving clinical outcomes and procedural efficiency.

Looking ahead to 2025 and beyond, the outlook for intravascular visualization devices is marked by several key trends:

- Continued adoption of hybrid imaging systems that combine IVUS, OCT, and NIRS modalities, providing comprehensive vessel assessment in a single procedure.

- Expansion into emerging markets, particularly in Asia-Pacific and Latin America, where rising healthcare investments and increasing cardiovascular disease burden are driving demand.

- Greater integration of AI-driven analytics for automated image interpretation, lesion characterization, and decision support, as seen in recent collaborations between device manufacturers and digital health companies.

- Ongoing miniaturization and catheter design improvements, enabling access to smaller and more complex vessels.

In summary, the intravascular visualization device sector in 2025 is characterized by technological innovation, expanding clinical applications, and a strong pipeline of new products from established leaders such as Philips, Boston Scientific, Abbott, Terumo Corporation, and ACIST Medical Systems. These trends are expected to drive further market growth and improved patient outcomes in the coming years.

Market Size & Growth Forecast (2025–2030): CAGR Analysis

The global market for intravascular visualization devices is poised for robust growth between 2025 and 2030, driven by technological advancements, expanding clinical applications, and the rising prevalence of cardiovascular diseases. Intravascular visualization devices—primarily intravascular ultrasound (IVUS), optical coherence tomography (OCT), and near-infrared spectroscopy (NIRS) systems—are increasingly integral to interventional cardiology, enabling real-time, high-resolution imaging of vessel walls and plaque morphology.

Key industry leaders such as Philips, Boston Scientific Corporation, and Terumo Corporation continue to invest in R&D, launching next-generation devices with enhanced imaging capabilities and user-friendly interfaces. For example, Philips offers the CoreVision platform, integrating IVUS and iFR (instant wave-free ratio) modalities, while Boston Scientific Corporation markets the OPTICROSS IVUS and the Farapulse pulsed field ablation system, reflecting a trend toward multimodal and multifunctional platforms.

The market’s compound annual growth rate (CAGR) for 2025–2030 is projected to be in the high single digits, with estimates commonly ranging from 7% to 9%. This growth is underpinned by several factors:

- Increasing adoption of minimally invasive procedures, particularly in North America, Europe, and rapidly developing Asia-Pacific markets.

- Rising incidence of coronary artery disease and peripheral vascular disease, necessitating advanced diagnostic and therapeutic tools.

- Ongoing clinical evidence supporting the superiority of intravascular imaging over angiography alone for optimizing stent placement and improving patient outcomes.

- Regulatory approvals and reimbursement expansions in key markets, facilitating broader clinical use.

Emerging players and established manufacturers alike are focusing on product innovation, such as integration with artificial intelligence for automated image analysis and cloud-based data management. Terumo Corporation and Philips are also exploring portable and catheter-based solutions to expand point-of-care applications.

Looking ahead, the market outlook remains positive, with continued double-digit growth in emerging economies and steady expansion in mature markets. Strategic collaborations between device manufacturers and healthcare providers are expected to accelerate technology adoption and training, further fueling market expansion through 2030.

Technological Innovations: From IVUS to OCT and Beyond

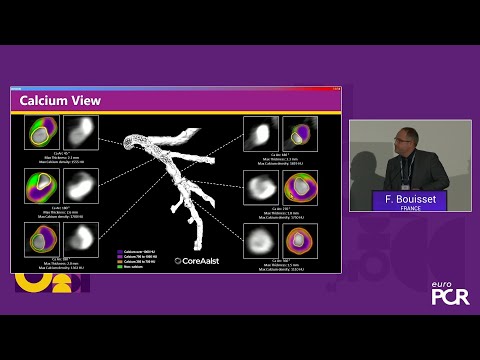

Intravascular visualization devices have undergone significant technological evolution, with the transition from intravascular ultrasound (IVUS) to optical coherence tomography (OCT) marking a pivotal shift in the field. As of 2025, these technologies are central to the diagnosis and management of coronary artery disease, peripheral vascular disease, and structural heart interventions. IVUS, which utilizes high-frequency sound waves to generate cross-sectional images of blood vessels, remains a foundational tool. However, the superior resolution of OCT, which employs near-infrared light, has driven its adoption for detailed assessment of vessel morphology, stent apposition, and plaque characterization.

Key industry players have been instrumental in advancing these modalities. Philips continues to lead with its Volcano IVUS and OCT platforms, integrating real-time imaging with advanced software analytics. Abbott has expanded its portfolio with the OPTIS™ Integrated System, which combines OCT and angiography co-registration, enabling precise lesion assessment and stent placement. Boston Scientific offers the POLARIS™ Multi-Modality Guidance System, supporting both IVUS and emerging imaging techniques, and is actively developing next-generation catheters with improved deliverability and image clarity.

Recent years have seen the emergence of hybrid and AI-enhanced platforms. Companies are integrating IVUS and OCT into single consoles, streamlining workflow and reducing procedure times. Artificial intelligence is being leveraged for automated plaque quantification, vessel sizing, and real-time decision support, with Philips and Abbott both investing in machine learning algorithms to enhance diagnostic accuracy and reproducibility.

Looking ahead, the next few years are expected to bring further miniaturization of imaging catheters, facilitating access to smaller and more tortuous vessels. The integration of intravascular imaging with robotics and remote navigation is also on the horizon, promising to improve procedural precision and safety. Additionally, the development of photoacoustic imaging and other novel modalities may offer complementary insights into plaque composition and vessel wall biology, expanding the clinical utility of intravascular visualization devices.

As reimbursement policies evolve and clinical guidelines increasingly endorse imaging-guided interventions, adoption rates are projected to rise globally. The convergence of high-resolution imaging, AI-driven analytics, and user-friendly platforms positions intravascular visualization devices at the forefront of precision cardiovascular care in 2025 and beyond.

Competitive Landscape: Leading Manufacturers & New Entrants

The competitive landscape for intravascular visualization devices in 2025 is characterized by a blend of established global manufacturers and a dynamic cohort of new entrants, each driving innovation in imaging modalities such as intravascular ultrasound (IVUS), optical coherence tomography (OCT), and emerging hybrid technologies. The sector is shaped by ongoing advancements in device miniaturization, image resolution, and integration with interventional platforms, as well as strategic partnerships and acquisitions.

Among the leading manufacturers, Philips maintains a dominant position, leveraging its extensive portfolio of IVUS and OCT systems, including the well-known Volcano and iFR platforms. Philips continues to invest in artificial intelligence (AI)-driven image analysis and workflow integration, aiming to enhance procedural efficiency and diagnostic accuracy. Boston Scientific is another major player, with its OptiCross IVUS catheters and the POLARIS imaging platform, focusing on user-friendly interfaces and real-time data integration to support complex coronary and peripheral interventions.

Terumo Corporation has expanded its global reach, particularly in Asia and Europe, with its high-resolution IVUS systems and a growing suite of complementary interventional devices. The company emphasizes seamless compatibility between imaging and therapeutic tools, a trend increasingly favored by clinicians. Cardiovascular Systems, Inc. (CSI), now part of Abbott, is also active in the space, integrating imaging with atherectomy and other plaque-modification technologies.

New entrants and smaller innovators are making notable inroads, often focusing on next-generation imaging modalities or AI-powered analytics. ACIST Medical Systems is recognized for its HDi IVUS system, which offers high-definition imaging and user-centric design. Meanwhile, companies such as Intravascular Imaging, Inc. (if confirmed operational) and other startups are exploring hybrid IVUS-OCT platforms and advanced software for automated lesion assessment.

The competitive outlook for the next few years is expected to intensify as regulatory approvals for novel devices accelerate, particularly in the U.S., Europe, and Asia-Pacific. Strategic collaborations between device manufacturers and digital health companies are anticipated to further enhance the clinical utility of intravascular visualization, with a focus on personalized medicine and data-driven decision support. As reimbursement frameworks evolve and clinical guidelines increasingly endorse imaging-guided interventions, both established leaders and agile newcomers are poised to benefit from expanding adoption across cardiology and peripheral vascular specialties.

Clinical Applications & Evolving Use Cases

Intravascular visualization devices, such as intravascular ultrasound (IVUS), optical coherence tomography (OCT), and near-infrared spectroscopy (NIRS), are increasingly integral to modern cardiovascular interventions. As of 2025, these technologies are being adopted more widely in clinical practice, driven by their ability to provide real-time, high-resolution imaging of vessel walls and plaque morphology, which is critical for optimizing percutaneous coronary interventions (PCI) and other endovascular procedures.

The primary clinical application remains in coronary artery disease (CAD) management, where IVUS and OCT guide stent placement, assess lesion severity, and evaluate stent apposition and expansion. Recent years have seen a shift from selective to more routine use of these devices, particularly in complex cases such as left main disease, bifurcation lesions, and chronic total occlusions. This trend is supported by growing evidence that intravascular imaging-guided PCI can reduce adverse cardiovascular events compared to angiography alone.

Key industry players are actively advancing the field. Philips offers the Volcano IVUS and OCT platforms, which are widely used in both research and clinical settings. Abbott provides the OPTIS Integrated System, combining OCT and angiography co-registration, and is also a leader in NIRS technology with its LipiScan system. Boston Scientific markets the iLab IVUS system and is investing in next-generation imaging catheters. These companies are also exploring artificial intelligence (AI) integration to automate image interpretation and enhance diagnostic accuracy.

Beyond coronary interventions, intravascular visualization devices are finding new applications in peripheral artery disease (PAD), structural heart interventions (such as transcatheter aortic valve replacement), and neurovascular procedures. The ability to characterize plaque composition and vessel architecture is particularly valuable in tailoring therapies and predicting procedural outcomes. For example, the use of IVUS in endovascular aneurysm repair (EVAR) is expanding, as it allows for precise device sizing and placement.

Looking ahead, the next few years are expected to bring further miniaturization of imaging catheters, improved integration with robotic and navigation systems, and expanded use in ambulatory and outpatient settings. The convergence of imaging modalities—such as hybrid IVUS-OCT catheters—and the incorporation of AI-driven analytics are poised to enhance workflow efficiency and clinical decision-making. As reimbursement policies evolve and clinical guidelines increasingly endorse intravascular imaging, adoption rates are likely to accelerate, solidifying these devices as standard tools in interventional practice.

Regulatory Environment & Standards (FDA, CE, etc.)

The regulatory environment for intravascular visualization devices—such as intravascular ultrasound (IVUS), optical coherence tomography (OCT), and near-infrared spectroscopy (NIRS) systems—remains dynamic in 2025, reflecting both technological advances and evolving clinical needs. In the United States, the Food and Drug Administration (FDA) continues to regulate these devices as Class II or Class III medical devices, depending on their intended use and risk profile. Most IVUS and OCT systems are cleared via the 510(k) premarket notification pathway, requiring demonstration of substantial equivalence to predicate devices. However, devices with novel features or new indications may require more rigorous premarket approval (PMA), especially as artificial intelligence (AI) and advanced analytics become integrated into imaging platforms.

The FDA has recently emphasized the importance of robust clinical evidence and post-market surveillance for intravascular imaging devices, particularly those incorporating AI-driven decision support. In 2024 and 2025, several manufacturers, including Philips and Boston Scientific, have announced new or updated regulatory clearances for their IVUS and OCT platforms, reflecting ongoing innovation and adaptation to regulatory expectations. The FDA’s Digital Health Center of Excellence is also increasingly involved in reviewing software components and cybersecurity aspects of these devices.

In Europe, the regulatory landscape has shifted significantly with the full implementation of the Medical Device Regulation (MDR, Regulation (EU) 2017/745). The MDR imposes stricter requirements for clinical evaluation, post-market surveillance, and traceability compared to the previous Medical Device Directive (MDD). As a result, manufacturers such as Terumo Corporation and ACIST Medical Systems have invested in expanded clinical studies and enhanced technical documentation to maintain or renew CE marking for their intravascular imaging products. The MDR’s focus on real-world evidence and unique device identification (UDI) is expected to improve patient safety but has also increased the regulatory burden and time-to-market for new devices.

Globally, regulatory harmonization efforts continue through organizations such as the International Medical Device Regulators Forum (IMDRF), which is working to align standards for software, cybersecurity, and clinical evaluation. In Asia, countries like Japan and China are updating their own regulatory frameworks to reflect international best practices, with agencies such as the Pharmaceuticals and Medical Devices Agency (PMDA) in Japan playing a key role in device approvals.

Looking ahead, the regulatory environment for intravascular visualization devices in 2025 and beyond will likely be shaped by the increasing integration of digital health technologies, the demand for real-world clinical data, and ongoing efforts to harmonize standards across regions. Manufacturers will need to remain agile, investing in compliance infrastructure and proactive engagement with regulators to ensure continued market access and patient safety.

Regional Market Dynamics: North America, Europe, Asia-Pacific

The global market for intravascular visualization devices—encompassing technologies such as intravascular ultrasound (IVUS), optical coherence tomography (OCT), and near-infrared spectroscopy (NIRS)—is experiencing dynamic regional shifts as of 2025. North America, Europe, and Asia-Pacific each present distinct trends shaped by healthcare infrastructure, regulatory environments, and adoption rates of advanced cardiovascular imaging.

North America remains the largest and most mature market for intravascular visualization devices. The United States, in particular, benefits from a high prevalence of cardiovascular disease, robust reimbursement frameworks, and rapid integration of new technologies into clinical practice. Leading manufacturers such as Philips and Boston Scientific Corporation have established strong distribution networks and ongoing clinical collaborations with major cardiac centers. The recent FDA clearances for next-generation IVUS and OCT systems have further accelerated adoption, with hospitals increasingly integrating these modalities into routine percutaneous coronary intervention (PCI) workflows. Canada, while smaller in market size, follows similar trends, with growing investments in digital health and imaging infrastructure.

Europe is characterized by a diverse regulatory landscape and varying levels of technology uptake across countries. Western European nations such as Germany, France, and the United Kingdom are at the forefront, driven by well-funded public healthcare systems and a strong emphasis on evidence-based medicine. The European Union’s Medical Device Regulation (MDR), fully implemented in 2021, continues to shape market entry strategies for device manufacturers. Companies like Terumo Corporation and Philips have expanded their European operations, leveraging local clinical trials and partnerships with academic hospitals. Central and Eastern Europe are witnessing gradual growth, supported by EU funding and increasing awareness of advanced cardiovascular imaging.

Asia-Pacific is emerging as the fastest-growing region for intravascular visualization devices, propelled by rising cardiovascular disease incidence, expanding healthcare access, and government initiatives to modernize hospital infrastructure. Japan, home to innovators such as Terumo Corporation</a), leads in early adoption and domestic manufacturing. China and India are rapidly scaling up, with local players entering the market and multinational companies investing in training and education programs for interventional cardiologists. Regulatory harmonization efforts and the proliferation of large-scale cardiovascular centers are expected to further boost regional demand through the late 2020s.

Looking ahead, North America will likely maintain its leadership in clinical adoption and innovation, while Europe’s regulatory rigor and Asia-Pacific’s demographic momentum will drive global market expansion. Strategic collaborations, local manufacturing, and tailored training initiatives are expected to shape the competitive landscape across all three regions.

Adoption Drivers: Precision Medicine & Minimally Invasive Trends

The adoption of intravascular visualization devices is accelerating in 2025, driven by the convergence of precision medicine and the ongoing shift toward minimally invasive procedures. These devices, which include intravascular ultrasound (IVUS), optical coherence tomography (OCT), and near-infrared spectroscopy (NIRS) systems, are increasingly recognized as essential tools for real-time, high-resolution imaging of vascular structures during diagnostic and interventional procedures.

A primary driver is the global emphasis on precision medicine, which demands tailored therapeutic strategies based on individual patient anatomy and pathology. Intravascular visualization devices enable clinicians to assess plaque morphology, vessel size, and lesion characteristics with unprecedented accuracy, supporting more personalized and effective interventions. For example, IVUS and OCT technologies are now routinely used to guide percutaneous coronary interventions (PCI), optimizing stent placement and reducing the risk of restenosis or stent thrombosis. This aligns with the broader healthcare trend of improving patient outcomes while minimizing unnecessary interventions.

The minimally invasive trend is another significant catalyst. Hospitals and health systems are prioritizing procedures that reduce patient trauma, shorten recovery times, and lower complication rates. Intravascular visualization devices facilitate these goals by providing detailed intraluminal images without the need for open surgery. This is particularly relevant in cardiology, peripheral vascular, and neurovascular interventions, where device-guided procedures are associated with improved safety profiles and faster patient throughput.

Major industry players are responding to these trends with continuous innovation. Philips has expanded its portfolio with advanced IVUS and OCT platforms, integrating artificial intelligence (AI) for automated image interpretation and workflow optimization. Boston Scientific is advancing its suite of imaging catheters, focusing on user-friendly interfaces and compatibility with a broad range of interventional tools. Abbott continues to invest in OCT and NIRS technologies, emphasizing their role in complex lesion assessment and decision-making during PCI. These companies are also collaborating with healthcare providers to generate robust clinical evidence supporting the value of intravascular imaging in routine practice.

Looking ahead, the adoption of intravascular visualization devices is expected to deepen as reimbursement policies evolve to recognize their clinical and economic benefits. Integration with digital health platforms and AI-driven analytics will further enhance their utility, enabling real-time decision support and longitudinal patient monitoring. As precision medicine and minimally invasive care remain central to healthcare strategies, intravascular visualization devices are poised to become standard of care across a widening array of vascular interventions.

Challenges & Barriers: Cost, Training, and Integration

Intravascular visualization devices, such as intravascular ultrasound (IVUS) and optical coherence tomography (OCT), are increasingly recognized for their ability to enhance diagnostic accuracy and guide complex cardiovascular interventions. However, as of 2025, several challenges and barriers continue to impede their widespread adoption, particularly in terms of cost, training, and integration into clinical workflows.

Cost remains a significant barrier for many healthcare systems. The initial investment in intravascular visualization platforms, including the capital cost of consoles and the recurring expense of disposable catheters, can be substantial. For example, leading manufacturers such as Philips and Boston Scientific offer advanced IVUS and OCT systems, but the price point often limits access, especially in resource-constrained settings. Additionally, reimbursement policies for these procedures vary widely by region, and in some markets, the lack of dedicated reimbursement codes further discourages routine use.

Training is another critical challenge. The effective use of intravascular visualization devices requires specialized skills in both image acquisition and interpretation. Despite efforts by manufacturers such as Abbott—which provides training programs and simulation tools for its OCT platforms—there remains a learning curve for interventional cardiologists and support staff. The need for ongoing education is heightened by the rapid evolution of device technology and software, which can outpace the ability of clinical teams to stay current.

Integration into existing clinical workflows also presents hurdles. In busy catheterization laboratories, the addition of intravascular imaging can increase procedure time and complexity. Seamless integration with other imaging modalities and hospital information systems is not always straightforward, particularly when devices from different manufacturers are used. Companies like Terumo Corporation and GE HealthCare are working to improve interoperability and user interfaces, but standardization across platforms remains limited.

Looking ahead, the outlook for overcoming these barriers is cautiously optimistic. Industry leaders are investing in cost-reduction strategies, such as reusable components and streamlined workflows, while also expanding training initiatives through digital platforms and remote proctoring. Advances in artificial intelligence and automation may further simplify image interpretation and integration, potentially reducing the expertise required and minimizing workflow disruption. However, the pace of adoption will likely remain uneven, shaped by local economic conditions, regulatory environments, and institutional priorities.

Future Outlook: Emerging Technologies & Strategic Opportunities

The landscape for intravascular visualization devices is poised for significant transformation in 2025 and the following years, driven by rapid technological advancements and strategic industry initiatives. Intravascular imaging, which includes modalities such as intravascular ultrasound (IVUS), optical coherence tomography (OCT), and near-infrared spectroscopy (NIRS), is increasingly integral to interventional cardiology and peripheral vascular procedures. The future outlook is shaped by a convergence of miniaturization, artificial intelligence (AI), and integration with therapeutic devices.

Key industry leaders such as Philips, Boston Scientific, and Terumo Corporation are actively investing in next-generation platforms. Philips continues to expand its portfolio with advanced IVUS and OCT systems, focusing on real-time, high-resolution imaging and seamless integration with cath lab informatics. Boston Scientific is advancing its OPTICROSS IVUS and POLARIS imaging platforms, emphasizing workflow efficiency and improved diagnostic accuracy. Terumo Corporation is also innovating in the field, particularly with its Ultimaster and Finecross product lines, which are designed for enhanced deliverability and precision in complex lesions.

Emerging technologies are expected to further revolutionize the sector. AI-powered image analysis is anticipated to become mainstream, enabling automated plaque characterization, vessel sizing, and real-time decision support. Companies are developing software that leverages machine learning to assist clinicians in interpreting complex imaging data, reducing variability and improving outcomes. Additionally, the integration of intravascular imaging with therapeutic devices—such as drug-eluting stents and atherectomy systems—will likely become more prevalent, supporting personalized and lesion-specific interventions.

Another strategic opportunity lies in the development of hybrid imaging catheters that combine multiple modalities (e.g., IVUS-OCT or IVUS-NIRS) within a single device. This approach aims to provide comprehensive vessel assessment, combining structural and compositional information to guide therapy. Several manufacturers are pursuing this direction, with prototypes and early clinical studies underway.

Looking ahead, the adoption of intravascular visualization devices is expected to accelerate, driven by expanding clinical evidence, guideline endorsements, and reimbursement improvements. The Asia-Pacific region, in particular, is projected to see robust growth due to rising cardiovascular disease prevalence and increasing investment in healthcare infrastructure. As regulatory pathways become more streamlined and digital health integration advances, the sector is set for continued innovation and broader clinical adoption through 2025 and beyond.

Sources & References